If you’ve seen the 1946 classic It’s a Wonderful Life, you’ve seen one of the most familiar examples of what happens when liquidity is promised against assets that cannot easily be turned into cash: a bank run, with crowds demanding money from an institution that does not have it on hand. This asset–liability mismatch - short-term liquidity promises funding long-term, illiquid investments - is a risk as old as banking itself.

While bank runs are the classic example, modern finance has repeatedly seen this same tension surface in other forms - across hedge funds, levered trading strategies, real estate vehicles, and reinsurance or credit structures. From Long-Term Capital Management in 1998, to Lehman Brothers in 2008, and most recently Silicon Valley Bank’s collapse in 2023, the pattern has been consistent: liquidity mismatches can appear manageable in calm markets, then become decisive when conditions tighten. Today, we believe a modern version of that risk may be emerging in private credit - particularly within so-called semi-liquid fund structures -and it has begun to attract headlines.

In this spotlight, we explain why, at Baker Street Advisors, we have been reluctant to recommend semi-liquid fund structures for holding private credit or direct lending assets, despite the operational conveniences they can offer. Our caution is driven less by the underlying asset class (though we do have concerns about certain segments of the market) and more by the structural risks created by liquidity promises layered on top of inherently illiquid investments.

Key Takeaway: We recommend accessing private credit through traditional closed-end drawdown funds that embrace illiquidity rather than mask it. Semi-liquid credit funds promise periodic liquidity on top of illiquid loans - an asset-liability mismatch that can end in gates, prorations, or forced selling when markets stress.

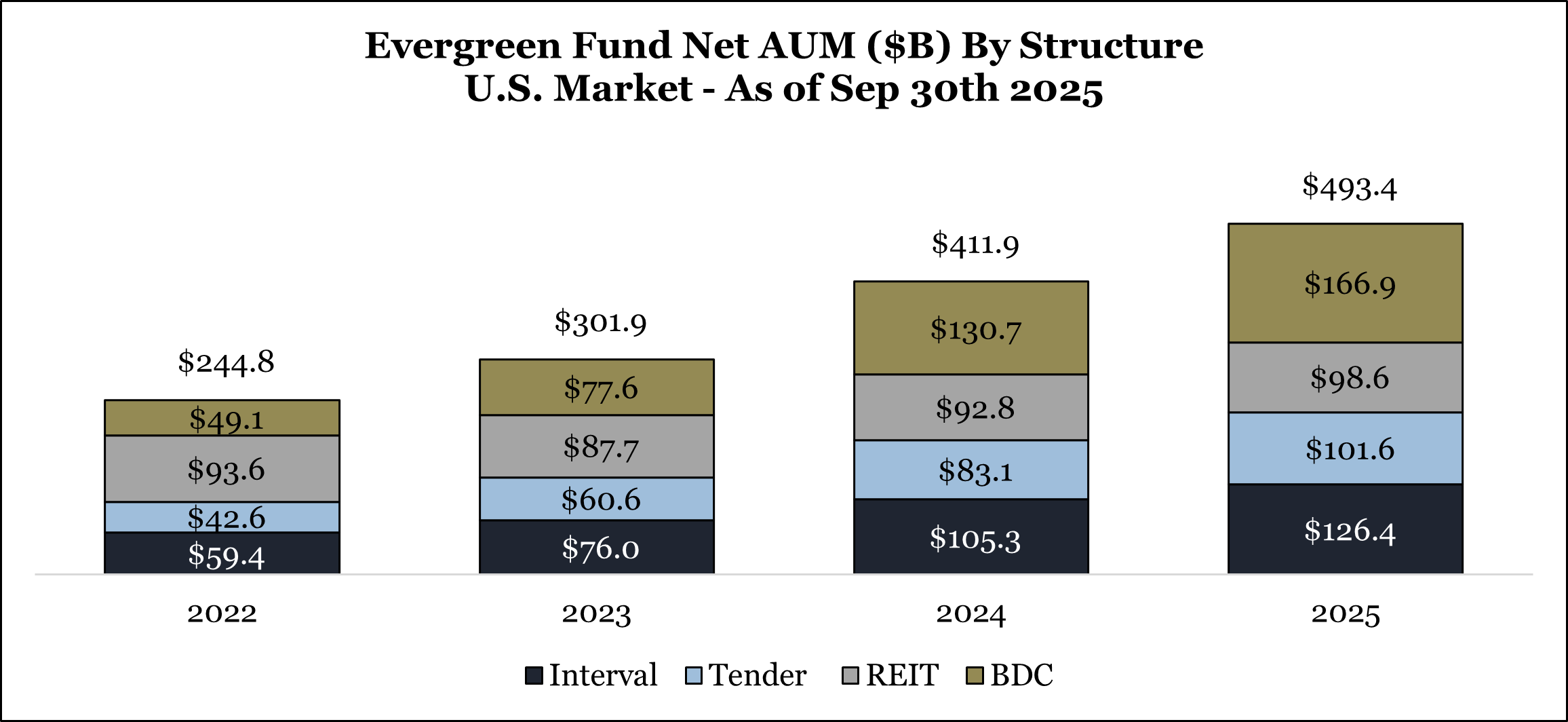

Semi-liquid investment funds are vehicles that package illiquid assets - such as private loans - into a structure that offers periodic redemption windows. They’ve surged in popularity as a gateway to private credit, particularly for retail and high-net-worth investors seeking higher yields with some degree of liquidity. According to PitchBook, as of September 2025, U.S. evergreen funds managed approximately $500 billion in assets, with direct lending and private credit representing more than half that total. This demand has been matched by rapid product growth: the number of U.S. registered evergreen funds increased from 149 in 2019 to more than 505 in 20251.

Within this broader expansion, non-traded perpetual BDCs(Business Development Companies) — often referred to as “perpetual BDCs” — have been a standout driver of investor flows. Cliffwater has noted that as of May2025, there are nearly 40 perpetual BDCs in existence and that they have gathered $127 billion in net assets over the last four years, surpassing the $112 billion in net assets across all other BDCs combined.2

What’s driving the appeal? Semi-liquid private credit funds “promise” the best of both worlds: access to portfolios of private, high-yield loans alongside liquidity via regular redemption windows. Unlike traditional private funds — where investors typically lock up capital for seven to ten years or longer and commit money that is drawn and invested over time — these vehicles generally put capital to work on day one while offering periodic redemptions (often quarterly). This steady inflow, however, can pressure managers to deploy capital quickly just to accommodate flows, rather than genuinely pursuing the most attractive opportunities. At the same time, liquidity is still meaningfully constrained relative to mutual funds with daily redemptions, creating a middle ground that offers some flexibility while allowing managers to hold less-liquid, higher-yielding assets.

Investors have been drawn to the pre-tax yields that often exceed those of public-market bond funds, as well as features such as daily NAV reporting and the ability to purchase shares easily online, which create an impression of mutual-fund-like convenience. The broader democratization of private markets — opening access to loans made to mid-sized or unrated companies — combined with a persistent search for income, has made these funds a popular pitch to individual investors.

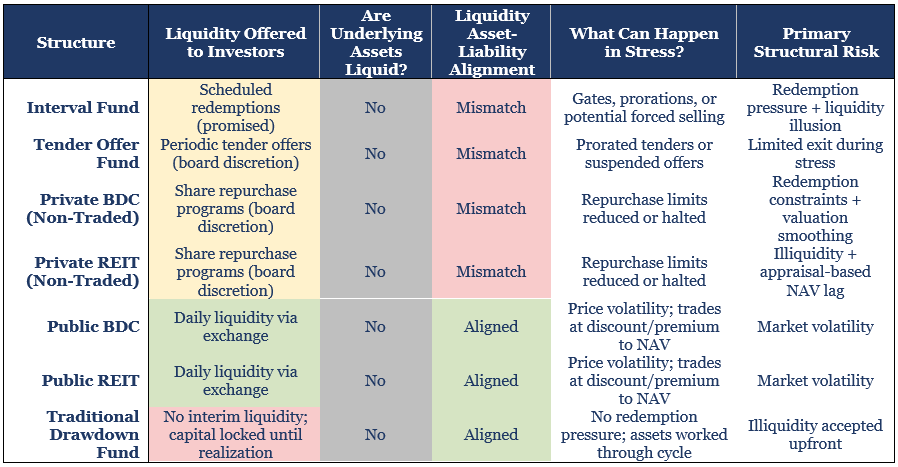

Beneath these attractive features lies a simple conflict: the funds offer periodic liquidity, but the assets they own are not liquid. That mismatch creates two key interrelated risks. First, illiquidity: when you want your money back — often during periods of market stress — your ability to exit may depend not just on the portfolio, but on other investors’ behavior and whether there is sufficient capital in the fund to meet redemptions. Second, forced selling: if redemption pressure persists, managers may be pushed to sell loans at stressed levels, potentially locking in losses and disadvantaging remaining investors.

By “illiquid,” we don’t mean an asset cannot be sold at any price. Rather, we mean that it may be difficult to raise cash quickly, in meaningful size, and at or near stated value without accepting a material discount. In private credit, secondary markets can be limited, and in periods of stress, positions may trade well below carrying values.

A useful — though imperfect — analogue is the exchange-traded BDC market: BDCs hold largely senior loan-based portfolios, yet their shares can trade materially below reported net asset value when conditions tighten. For example, a widely followed index — the Cliffwater BDC Index — reflects a price-to-NAV of roughly 0.78x as of February 27th (a 22% discount to stated NAV).3 This discount is the market’s way of pricing liquidity and uncertainty — investors are effectively saying with their dollars, “we’re only willing to own this portfolio of loans at a meaningful markdown.” It’s a reminder that converting similar assets to cash under stressed conditions may require accepting significant price concessions relative to stated NAV. The key difference, however, is that public BDCs do not offer redemptions: investors who want liquidity sell their shares to other investors in the market, so the BDC isn’t forced to sell loans to fund withdrawals.

Importantly, it’s not only the “back end” (redemptions) that gives us pause. The “front end” can be just as challenging: these open-ended, perpetual structures often rely on continuous capital raising, and managers are incentivized to deploy new inflows quickly to keep their funds fully invested and maintain distribution targets. That can create pressure to put money to work when spreads are unattractive or underwriting standards are weakening — particularly if inflows remain strong even as the opportunity set deteriorates.

Most semi-liquid private credit funds cap redemptions at a fixed percentage of NAV during each redemption window (often around 5% per quarter, sometimes higher). These limits are intended to slow outflows and protect the portfolio, but they also mean investors do not have on-demand access to their capital — a distinction that can be easy to miss amid marketing that emphasizes “liquidity.” In practice, these funds should be approached with the expectation that capital may be inaccessible for extended periods, particularly when liquidity is most valuable.

The structure functions smoothly as long as inflows remain strong or at least stable. Redemptions are typically funded through a combination of loan repayments, interest income, credit facilities, and —critically — ongoing subscriptions from new investors. If flows reverse, managers may be forced to prorate withdrawals or gate redemptions, and prolonged pressure can ultimately lead to asset sales into stressed markets —often at meaningful discounts to intrinsic value. Compounding this risk, many funds have limited live stress-test history. We are not suggesting these outcomes are inevitable, but we believe the combination of illiquidity risk and the potential for forced selling is a meaningful tradeoff that is difficult to justify in exchange for the operational convenience these structures provide.

Borrowing short and lending long has always carried risk - this is simply a modern flavor of this dynamic. Whether it’s George Bailey pleading with depositors in a black-and-white film that their money is in “Joe’s house and the Kennedy house” (not sitting in the vault), or a fund manager balancing quarterly redemption requests against multi-year loans, the underlying principle is the same. The core vulnerability is an asset–liability mismatch that no amount of structuring or marketing can fully eliminate. If too many investors head for the exits at once, managers may be forced to sell assets into stressed markets or impose redemption gates - an outcome we’ve already seen in other “illiquid but redeemable” vehicles.

None of this means semi-liquid private credit funds are “bad” or destined to fail. With strong management and realistic expectations, they can play a role in portfolios that otherwise may not be able access private, floating-rate loans that may improve returns and diversification. The key is to treat them for what they are: long-term, illiquid investments, not ETF-like products you can trade in and out of freely.

For investors, our takeaway is simple: these structures come with restricted exits, added risk, and the real possibility that liquidity disappears precisely when you want it most. From our perspective, clients are better served by accessing these strategies through structures that are less vulnerable to liquidity mismatches and that avoid the added risks and distractions of managers having to simultaneously manage portfolios and investor flows.